In January of 2023, inflation began to cool, and Canada’s top banker, Tiff Macklem, boasted that “it’s working” about higher interest rates…

Eight months later, inflation remains stubbornly above target (2%), with July’s CPI coming in at 3.3%. Result: many Canadians are getting poorer.

And, despite the Bank of Canada pausing on rates after pushing the key rate to 5% during the summer, don’t expect rate cuts anytime soon.

To his credit, Macklem knew the job was a long way from finished. He was honest with the Canadian public, stating,

“But I don’t want to pretend that it’s painless. It’s not painless.”

And, ”it’s not going to feel good.”

It now feels so bad, in fact, that Ontario and BC’s premiers recently wrote letters to the central bank, begging them to stop raising rates. Both Doug Ford and David Eby spoke of the crushing effect higher rates are having on households within their provinces.

Is it a coincidence that Ontario and BC are home to Canada’s most expensive real estate markets, where many homeowners over the past 10 years have overextended themselves?

After this week’s pause in rate increases, Canadian Finance Minister Chrystia Freeland, in a rare statement regarding monetary policy, said it was welcomed relief…

The Liberals know their political future likely hinges on an easing of monetary policy.

Interest Payments Top $146 Billion in Q1 of 2023

One of the most unproductive things you can spend money on is interest from debt…

According to Stats Canada, households’ total interest paid in Q1 of 2022 totaled $93.44 billion. In Q1 of 2023, that number grew to $146.20 billion and will have increased even more when Q2 data for 2023 is released.

Bankers are getting rich as households that took on too much debt or failed to pay debt off during the good years are feeling the heat.

So yes, an extra $60 billion (YoY) in interest doesn’t feel great.

As a band-aid solution, amortization periods are soaring along with the variable rate, so those who selected a ‘fixed-payment’ variable rate now see their principal payment effectively vanish. They are virtually ‘renting their home’ from the bank and paying a hefty price to do it as amortizations extend to 70, 80, and even 90 years, according to new data compiled by Clarrie Feinstein, a Business Reporter at the Toronto Star. But, when the term expires, these borrowers could be in for a world of hurt.

Homeownership in Canada fell to 66.5% in 2022 – a 20-year low. Its all-time high was reached in 2019 at 68.6%. This is a massive decline in a very short period of time. And with home prices proving more resilient than expected, we may have witnessed ‘peak home ownership’ in Canada unless drastic policy changes are made at both the provincial and municipal levels.

Macklem’s Mortgage Timebomb

Every month, tens of thousands of mortgages come up for renewal in Canada. The shock is overwhelming for those who locked in at fixed rates in 2018, 2019, and 2020 (most below 2%)…

That extra $60 billion in interest collected by lenders is spread across millions of Canadians struggling to make their mortgage and car loans. Others who locked in just before the hiking cycle still have a year or two before their panic sets in.

But time is running out, and Canada’s central bank knows it. The more Canadians are forced to renew and pay higher and higher rates, the greater the systemic risk to the broader economy, standard of living, fertility rate, etc.

Homeowners Extend and Pretend

As homeowners extend and pretend, the time will come when many must sell their homes and downsize. For some homeowners, that moment has already arrived. For others, it will come later this year or next. House prices rebounded to start the year, but that may be short-lived.

Record levels of immigration, asset inflation, and housing supply shortages keep prices elevated. However, if listings soar, values will tumble.

Canada’s economy has already rolled over…

Canadian GDP contracted by 0.2% on an annualized basis in Q2 of 2023, well below market expectations of a 1.2% expansion. Meanwhile, Canada’s productivity rate has fallen nearly every quarter over the past three years!

In our view, the Bank of Canada has about 9 to 12 months to begin cutting rates.

Low-Income Canadians Can’t Take Higher Interest Rates

Here is the demographic that will ultimately force Canada’s central bank and many other banks to change course. About half of Canadians live paycheck to paycheck – a stunning number. A recent survey published on September 1, 2023, from Leger, confirmed that 47% of Canadians and 46% of Americans live paycheck to paycheck.

And, for low-income households, the pain of not being able to afford necessities is far worse than paying an interest-only 90-year mortgage. Missing a car or mortgage payment is one thing, but going without food or shelter is another…

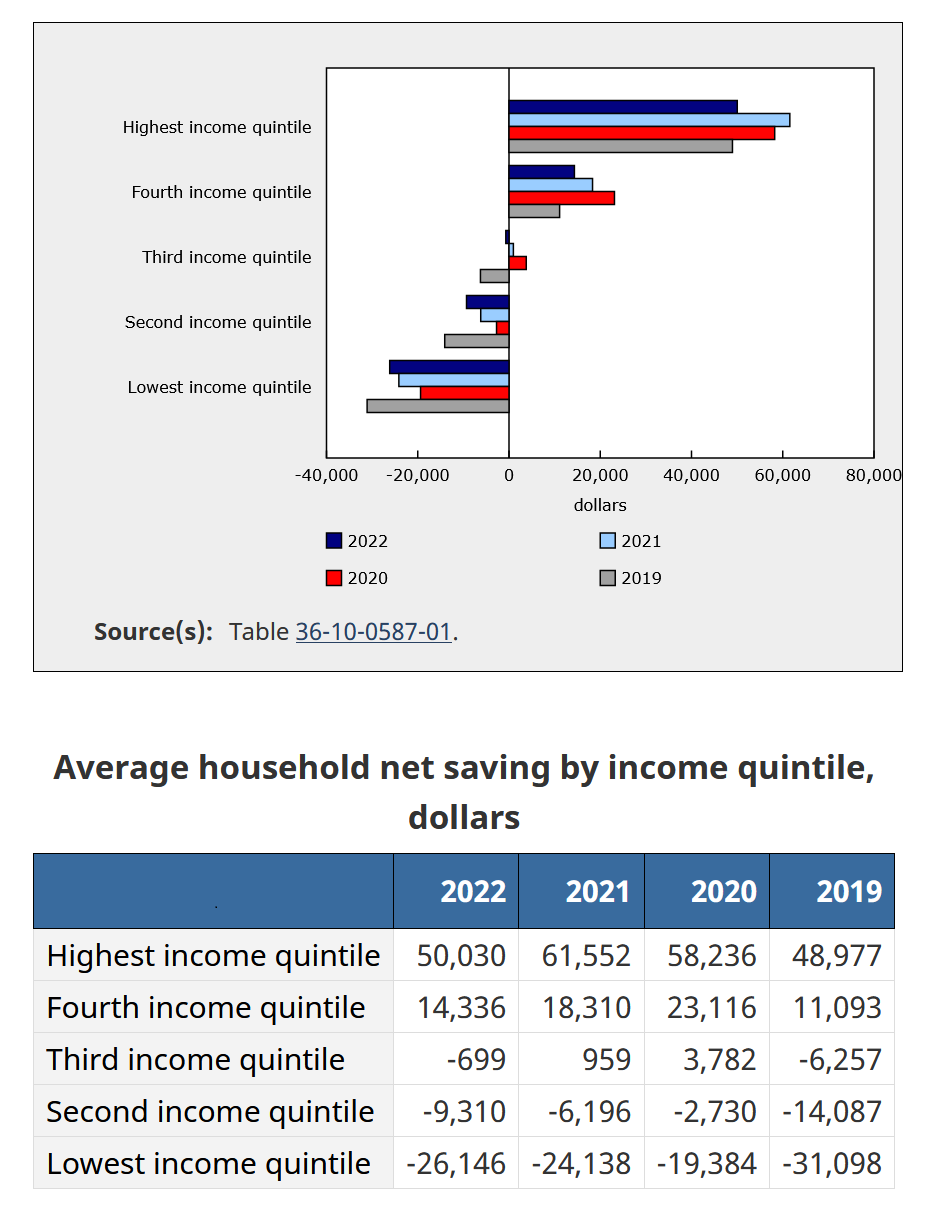

Negative Net Savings Becomes Widespread

According to Statistics Canada,

“…middle-income earners (third quintile) returned to negative net saving in 2022, meaning that, on average, these households spent approximately $700 more than they earned in income. The average net saving of households in the second income quintile decreased by 50.3%.”

Higher borrowing costs, taxes, maintenance, and utility costs force landlords to raise rents, leaving little or no savings for middle to low-income earners. Now, here is the final stat from Stats Canada that shows just how devastating inflation can be for low-income households,

“The least wealthy households were affected more by recent economic pressures, as they decreased their average net worth by 16.3% in the fourth quarter of 2022 relative to the same quarter a year earlier, more than triple the rate of decrease for the wealthiest households (-5.2%).”

Canada’s least wealthy households’ savings are evaporating or already gone. A 16% hit in net worth in one quarter? That is massive!

Average Household Net Saving by Income Quintile

What the Future Holds for Rates

The point of all this is to show just how serious things are getting for roughly 20 to 30 million Canadians. Canada’s central bank will keep rates elevated until core inflation drops below 3%. With energy prices rising, it could be a few more quarters…

The Recession is Here?

In the past half-century, we have only witnessed two such dramatic interest rate hike cycles: in the early 1980s, when rates soared more than 10% in about a year, and then between 1987 and 1990, when rates jumped more than 6%. In both those instances, the economy faltered and entered steep recessions while asset values dropped.

While the wealthiest households appear well-positioned, too many Canadians have over-extended themselves, and it is just a matter of time before that vacation property or primary residence hits the market.

In conclusion, debt servicing costs are becoming too much for many Canadians. We expect defaults to rise as 2023 progresses. The hangover from the 2021 and early 2022 boom is nowhere near over.

All the best with your investments,

PINNACLEDIGEST.COM