As the U.S. bond bull market confirms its end, spooking investors the world over, it’s time to prepare for a generational decline in bond prices. With bond yields rising, and their face value declining in many instances, the stock market sent a warning to equity investors this past week…

On Wednesday alone, the Dow Jones dropped over 800 points, more than a 3% decline. Then on Thursday, the collapsed continued, with the index losing more than 500 points, or roughly 2%. Concerns that rising interest payments will disrupt the status quo of historically low rates is sending the market into a tailspin. But yet, this environment, if controlled, is exactly what the Fed needs. More on this shortly.

Bond Bull Market Ends | The Good and the Bad

Signals the bond bull market’s best days are behind it have been flashing since the end of last year. Because of the length of bond cycles (they last decades, not years) investors must understand the wide-reaching impacts this reversal could have.

Today’s letter is designed to help you accept, if not welcome, the bursting of the near 36-year bond bubble, and the ramifications it will likely have. Remember, high bond prices (not high yields on bonds – two different things) are a result of low-interest rates; and, we are finally moving out of a period of historically low-interest rates, which means bond yields must rise – a detriment to equities.

On October 6th, MarketWatch published, A $20 trillion bond index is on track for its second-worst year in history. According to the article,

“The index is one of the most widely used barometers for bond-fund managers, and is associated with more than $20 trillion of assets.”

Year to date, The Bloomberg Barclays U.S. Aggregate Bond Index is down around 2.5% on a total return basis. This not only includes the value of bonds held in the basket, but the yields derived from those assets. To understand how historic the loss is, one has to look back to 1994 to find a worse performing year, a time when the index slipped around 2.9%.

So, why was 1994 such a bad year? According to the MarketWatch article,

“Highly leveraged investors dumped their holdings of government bonds in U.S. and Japan after the Fed started to raise rates in response to the U.S. economy’s upswing in the 1990-91 recession.”

Rising Interest Rates End Bond Bull Market | U.S. Economy Still Rolling

The current bull market in U.S. stocks is in uncharted territory. It is the longest in modern history. The economy is also nearing a historic mark – about six months from the all-time longest expansion (the 1991 to 2001 expansion is looking like it’s about to be knocked off). In short, the Fed is playing catch up and rates will climb still further from here.

In a March article from Bloomberg, Rising Treasury Yields Are a Good Problem to Have, the top five worries about rising rates are outlined:

- Principal losses in bonds

- Lower valuations in stocks because of competition from bond yields

- Higher inflation

- The end of the economic expansion

- Higher interest payments for corporations, governments, and individuals in debt

One could say that each worry comes with a positive flip side. As in any economic environment, there is money to be made. Understanding how to benefit from falling bond prices and rising interest rates is what investing in the next few years will likely be about…

We are already witnessing principal losses in bonds as investors begin to realize the bond bull market is over. The iShares Core U.S. Aggregate Bond ETF’s NAV Total Return as of October 11, 2018 YTD was -2.52%. This is a stark contrast to recent years of solid gains.

In a December article, One Chart That Shows The Bond Bull Market Is Over, published on Forbes, Rob Isbitts explains why the bond bull market is over:

“…it is over because bond rates and potential returns have reached the point where they no longer allow most investors to achieve their retirement goals. Today’s rates and the prospect of higher rates in the coming years are a mathematical long shot for bonds to deliver for investors as they have for so long.”

Risk-averse savers couldn’t be happier to see rates rising. According to a recent Bloomberg article,

“Marcus, the online bank run by Goldman Sachs, currently offers a five-year CD for 2.60 percent. In 2014, the average CD was paying closer to 0.79 percent, according to Bankrate.com.”

Access to low risk, rising and predictable returns is a total game-changer for many retirees, or those with a bearish outlook on equities given their historic highs in the US. Which brings us to Worry #2: Lower valuations in stocks because of competition from rising bond yields…

U.S. Stocks Under Pressure as Bond Yields Rise

This is a very real threat to the current US stock bull market – which last month reached historic levels. The S&P 500 closed down almost 3.5% Wednesday and another 2% Thursday, its sixth consecutive negative close. Clearly, the markets are concerned that rising interest rates will have a negative impact on stock prices. History has shown they do – and a recent CNBC article explained as much,

“Higher rates and expectations of tighter monetary policy are a drag on stock markets, given that they cap companies’ profits, thus restricting possible dividends to investors and higher pay for the employees.”

Before last week’s mini crash, U.S. stocks (S&P 500) were up about 11% since April. Many investors are justifiably arguing the correction was healthy, and inevitable. However, we want to remind those folks that the correction in stock prices came amidst the benchmark 10-year Treasury note yield touching its highest level since 2011, above 3%.

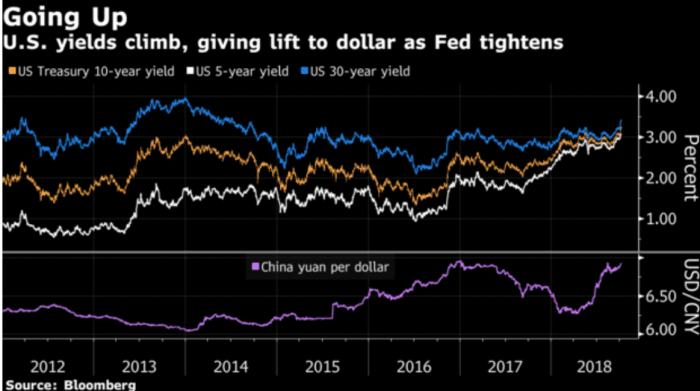

US Generic Government 10 Year Yield

The yield on the 10-year treasury bond is on fire after falling below 2% in 2016.

5, 10 and 30-year US Treasury bonds Moving Higher in Unison

Rising rates have strengthened the dollar while weakening other currencies, including the yuan. Thus, money is becoming more expensive – those up for mortgage renewals need no reminder.

Higher rates historically lead to Worry #4: The end of economic expansion. As it stands, the current economic expansion shows no signs of slowing. 3% GDP for the full year is expected in 2018 and 2019. Many of the top economic and market forecasters are not forecasting a recession until 2020. Still, continual rising rates (in the current environment it has been happening for roughly two years) almost always precede a recession; or at a minimum, a significant economic slowdown.

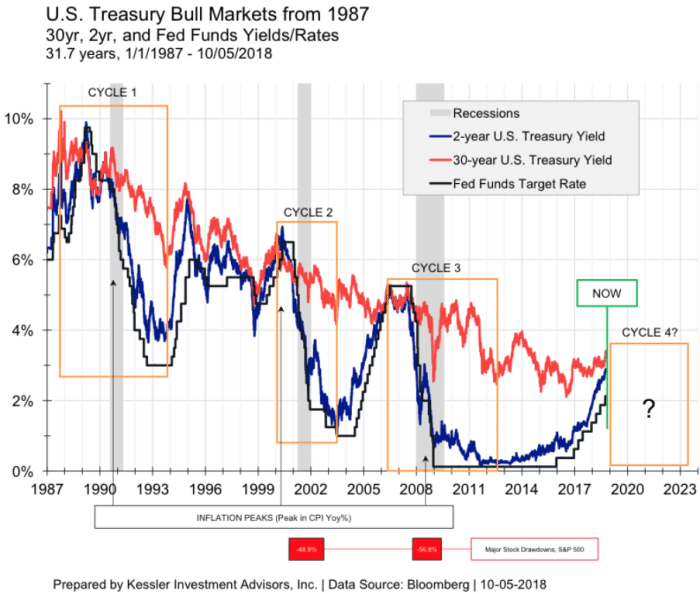

According to an October 9th Zero Hedge article,

“There have been three major U.S. Treasury bull markets coinciding with recessions in the last 30 years (orange boxed areas in the chart below). They all look remarkably similar and the periods leading up to them look a lot like now.”

By that, the Zero Hedge article implies that rising yields defines a U.S. Treasury bull. Which, of course, takes liquidity from equities.

Eric Hickman, President of Kessler Investment Advisors, an advisory firm located in Denver, Colorado specializing in U.S. Treasury bonds, continued,

“It is counterintuitive, but U.S. Treasury bull markets begin when the economic weather is the sunniest. It happens when the unemployment rate is the lowest and consumer and industrial confidence the highest. By the time a recession is obvious, a good chunk of the move lower in rates will have taken place.”

Interest Rates and Higher Inflation

The third and sometimes most troubling worry about rising rates is their association with higher inflation. For years, some economists warned the Fed was keeping interest rates too low for too long. They argued that debt monetization and historical currency creation would lead to hyperinflation. This is very unlikely as the Fed continues to deleverage while raising rates.

The Fed, for all intents and purposes, is working its game plan to perfection. And its plan does not involve anything remotely close to hyperinflation.

That stated, the Trump Administration and Republicans are spending at a pace similar to Obama. The President is pushing for record spending on the military and is forgoing tax revenue from America’s largest companies believing the economy will continue to benefit.

While one-quarter of +4% GDP is nice (Q2, 2018), Trump (and America as a whole) will need to string together years of solid growth before the deficit significantly (and continually) declines. There’s a reason we dubbed him The Inflation President, on November 13th, 2016 – just days after winning the most historic election in our lifetime.

US Inflation Upticks Under President Trump

So, with the Fed’s inflation gauge finally hitting its target for the first time since 2012, and the U.S. economy booming, further rate hikes should keep inflation range bound.

All Part of the Fed’s Plan

Remember how the hyperinflation crowd said the Fed would never be able to unwind its balance sheet? They were wrong. The Fed is doing just that, and the rising rate environment it has created will continue to facilitate this. With increasing bond yields (by increasing interest rates) the Fed is essentially grabbing liquidity from stocks and inserting it into the bond market – further enabling its deleveraging plan…

After ballooning to $4.5 trillion and staying there for years, the Fed is finally reducing its balance sheet. While still a tall order, rising yields are making bonds more attractive to investors. Check out the last year of the Fed’s balance sheet reduction below…

That’s nearly a 10% reduction in under 12 months.

From $4.5 trillion in January of 2016, the Fed’s balance sheet has grinded lower to $4.17 trillion on October 1st. Virtually all of that reduction has occurred in 2018. A drop below $4 trillion by early next year would be impressive. Bookmark the chart above and keep a close watch on it over the coming months.

The Biggest Worry of Them All

With the Fed stepping out of the U.S. Treasury market, some major market players are worried demand will suffer. Herein lies the balancing act for the Fed of “how much, how soon” when it comes to unwinding that monstrous balance sheet.

“It is unclear whether sufficient demand exists to soak up the supply, with government debt sales estimated to reach $1.3 trillion in 2018, more than double last year’s figure.”

Free Money Tap Runs Dry for Corporations

In a Financial Post piece from June on the state of US corporate debt, titled, The ‘mother of all credit bubbles’ is brewing – and this time it isn’t household debt, the danger of cheap money is exposed,

“Rather, it is giant corporations using cheap debt – and a one-time tax windfall – to take cash from their balance sheets and send it to shareholders in the form of increased dividends and, in particular, stock buybacks.”

Furthermore,

“Last year, public companies spent more than US$800 billion buying back their own shares and, thanks to all the cash freed up by the recent tax bill, Goldman Sachs estimates that share buybacks will surge to US$1.2 trillion this year.”

In late-2016, we warned of the impending consequence of corporate share buyback programs, stating the stock market was “kept afloat by low interest rates and share buyback programs fueled by debt.”

Expect buybacks to decline and corporations to slowly tighten their belts as rates rise. With cheap money coming to an end, investors have cause for concern when it comes to the fifth and final worry on higher interest payments for corporations, governments, and individuals in debt.

Wrapping Up

In all likelihood, the 10-Year Treasury will decline back below 3% before stabilizing and slowly moving higher again. The recent action in the bond market serves as a warning for investors to organize and prepare…

The Fed knows it needs wiggle room for the next recession, and thus finds itself in an incredible balancing act of tightening monetary policy while not tormenting the economy and giving it reason to contract. So far, it has executed with the utmost precision.

Trump understands the dynamic relationship between interest rates, the stock market and overall consumer sentiment. What’s more, how deeply important each are to the midterms and his reelection bid in 2020. He critiqued Powell and the Fed Wednesday morning, complaining about rising rates, by stating, “I don’t like it” and “I think we don’t have to go as fast.” On Thursday, he went as far as to call the Fed crazy, stating, “They are so tight. I think the Fed has gone crazy.”

Short term, with US midterms less than 30 days away, expect the markets to rise dramatically in November if Republicans maintain control of the House and Senate. Expect the opposite if Democrats win, as the news cycle will be filled with impeachment talk. Investors hate that kind of uncertainty. Over the longer term (12-18 months), however, bond yields will rise, putting pressure on equity valuations from small caps to large.

All the best with your investments,

PINNACLEDIGEST.COM

P.S. If you’re not already a member of our newsletter and you invest in CSE or TSX Venture stocks, what are you waiting for? Subscribe today. Only our best content will land in your inbox.