Gold stocks typically outperform gold during bull markets. One of the main reasons for this is the leverage associated with the ‘in-ground’ gold these mining companies (and even explorers) control.

In-ground gold (based on resource estimations or reserves) is essentially the amount of gold a company has defined (via the drill bit) on its land, but has never mined.

An In-Ground Gold Hypothetical

In-ground gold can very quickly go from being not valued, to undervalued, and then ultimately overvalued. Its value is highly speculative and largely depends on market sentiment.

Here is a hypothetical of how juniors can benefit from the leverage to gold’s price in a bull market via their in-ground gold:

A non-producing junior gold mining/exploration company might have 1 million ounces of estimated gold in the ground (NI 43-101 qualified resource(s) estimate in the Inferred, Indicated or Measured categories). During a bull market, when gold’s price jumps $20 (roughly 1% today), hypothetically the value of said junior’s in-ground gold just increased — somewhere in the range of an extra $0.25 – $0.75 per ounce is possible (based on $1,700 p/oz spot price). So, the asset value may have increased up to $750,000 that day — at least on paper.

Although $20 an ounce represents roughly a 1% increase in gold’s value, it can potentially increase the value of a junior gold company by up to 5% (sometimes even more). Many non-producing juniors with a resource estimate of roughly 1 million ounces have had less than a $20 million market cap in recent times. So, a $750,000 addition to the market cap represents nearly a 4% valuation uptick for the junior in this scenario.

Although that is oversimplified math, we use it to explain the potential for certain gold equities in a bull market for the precious metal. Investors often fail to grasp the positive impact a surging gold price can have on junior gold stocks — particularly when the viability of a development stage asset is believed to be positive.

The Discount is Massive

Understand that in-ground gold trades at a massive discount to the spot price of gold because there are question marks around whether it will ever be mined. Investors are also wary of the future dilution required to build a mine, the project’s long-term economics, potential environmental challenges, and several other variables/risks. Thus, a 99% discount (or more) to the spot price is not uncommon for in-ground gold at an exploration or development stage asset.

The Value of an In-Ground Ounce of Gold Varies

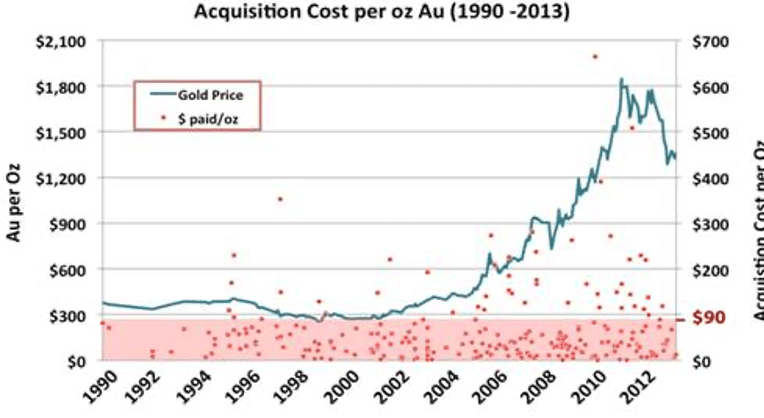

Below is an excerpt from a 2015 Kitco article, The Real Value of Gold in the Ground,

“Based on 253 gold deposits acquired from 1990-2013, Cipher calculated a median benchmark value for an ounce of gold in the ground at about $40 and established that 80% of the ounces were valued at less than $90.

Note that Cipher’s treatment includes all categories of 43-101 qualified resource estimates: measured, indicated, and inferred resources.”

Bull Market to Potentially Increase Amount Seniors Pay for In-Ground Gold

If the gold bull market continues, the amount paid for in-ground gold (via acquisitions) will likely increase.

Check out the below chart from Kitco which highlights the acquisition cost per ounce from 1990 to 2013.

Source: Kitco

The red dots represent the price paid per ounce in acquisition scenarios. While the vast majority of acquisitions took place below the $90 per ounce level, as the price of gold moved higher, more $90+ per ounce acquisitions occurred.

With gold’s price currently around $1,700, and the U.S. committed to unprecedented quantitative easing to stave off what is becoming the worst employment downturn since the Great Depression, the precious metal is in a bonafide bull market once again. How long it lasts is anyone’s guess, but we don’t see any near-term catalysts that could derail gold’s current bull run.

Let’s update you on one of our clients, a junior gold explorer and developer, which owns the second largest undeveloped gold deposit in Europe.

Euro Sun Mining

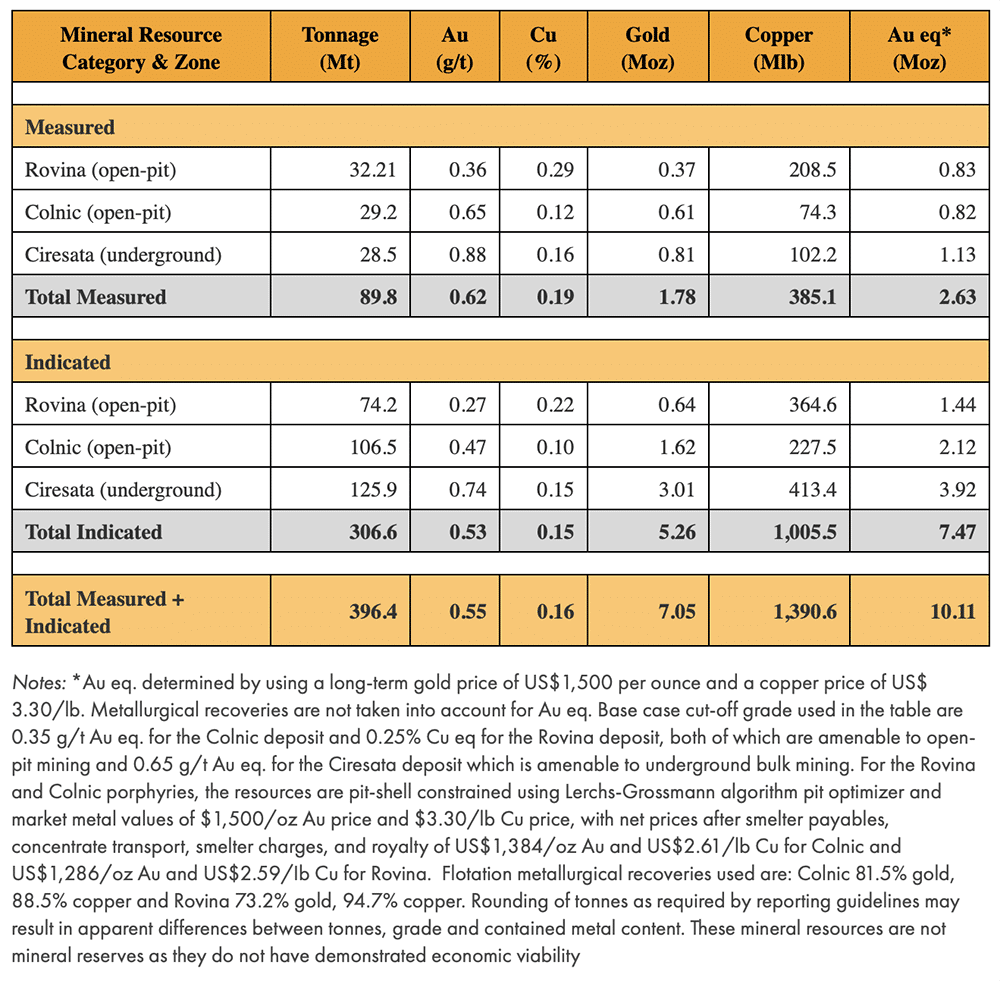

Euro Sun Mining (ESM: TSX) is developing the Rovina Valley Project in west-central Romania. The project has *measured & indicated mineral resources of 10.1 million ounces (combined) of gold equivalent (see details related to the mineral resources here). The resources are based on three porphyry deposits that define a north-northeast trend over a distance of 7.5 km.

- These Mineral Resources are not Mineral Reserves as they do not have demonstrated economic viability. Mineral Resource Estimates do not account for mineability, selectivity, mining loss and dilution. See other important disclosures pertaining to the Rovina Valley Project’s mineral resources estimates here.

When our crew visited Euro Sun’s Rovina Valley Project in Romania last year, President and CEO Scott Moore stated,

“On current prices, we’re trading at about 2.30 cents U.S. dollars an ounce.”

Euro Sun has invested roughly CAD$70 million in its flagship project over the past decade or so. Today, its market cap sits at CAD$43.04 million, according to Bloomberg. At the time of our introduction last September, and a couple months after CEO Scott Moore made the above comment, the company had a market cap of about CAD$31 million.

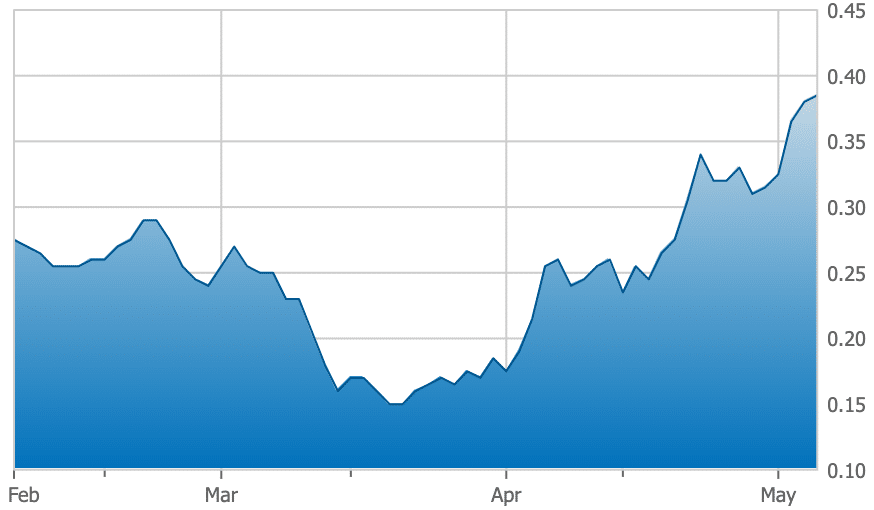

Euro Sun Mining – 3 Month Chart

Source: Quotemedia

Our exclusive video interview at Euro Sun’s Rovina Valley Project was filmed last June and released on September 6, 2019, when gold closed around $1,506 per ounce. Gold is up about $200 per ounce since then, yet Euro Sun’s share price is only up two pennies (approximately 5%).

Euro Sun Targets Construction Permit and the Definitive Feasibility Study in 2020

Euro Sun provided a corporate update and commented on its current strategy regarding development of its Rovina Valley Project on March 26th,

“The Company has two key milestones in progress for completion or substantial completion in 2020. The two targeted deliverables include the Construction Permit and the Definitive Feasibility Study. The current global COVID-19 crisis may have an impact on timing that currently is hard to predict, but we are confident that any delays may be minimal. These deliverables are significant risk reduction events for Euro Sun and should have a materially positive effect on the Company.”

Click here to read the full release.

On the Definitive Feasibility study, Euro Sun commented,

“The Company issued a formal request for proposal to several global engineering firms which have subsequently been received. We are currently evaluating said proposals and expect to award the contract shortly. After internal model evaluations the Definitive Feasibility Study will now include the Rovina open pit sequentially to the Colnic pit in the Life of Mine plan. This will result in a significantly more production of both gold and copper and a longer mine life without affecting initial capital expenditures.”

Click here to read the full release.

Highlighted Euro Sun News Since Pinnacle Digest Introduction

- Euro Sun Provides Corporate Update on Rovina Valley

- Euro Sun Closes Previously Announced Private Placement Financing

- Euro Sun Appoints Samuel Rasmussen as Chief Operating Officer for Rovina Valley

- Euro Sun Upsizes Previously Announced Private Placement Financing to $3.75 Million

- Euro Sun Appoints Bruce Humphrey to Board of Directors

- Euro Sun Awards Environmental Impact Assessment to Leading Global Consultants ERM International

- Euro Sun Discovers Four New Gold-Copper Porphyries Adjacent to Its Rovina Valley Project

- Euro Sun Appoints Mr. Danny Callow to Board of Directors

Wrapping Up

With the gold bull market appearing primed to continue as debt and money supply in the United States and much of the world expands, certain gold stocks have the potential to benefit.

Project valuations typically increase, at least in part, due to a rising gold price and heightened retail and institutional interest in gold stocks (and the precious metal itself).

Euro Sun has two key milestones in progress for completion or substantial completion in 2020. The two targeted deliverables include the Construction Permit and the Definitive Feasibility Study for its Rovina Valley Project — an asset described by the company as a “world-class gold development project.” If Euro Sun can achieve these deliverables/goals, and the price of gold continues to rise, the company could receive broader investor interest.

We hope this report provides a high-level overview of Euro Sun and its near term plans, but it is not intended to be exhaustive. Conduct your own thorough and independent due diligence to properly understand the risks associated with investing in a speculative company of this nature. A good place to start your due diligence is reviewing Euro Sun Mining’s Sedar filings at www.sedar.com. Euro Sun Mining is most certainly in the exploration and development stage, which at some point will likely result in further dilution to shareholders. Pick your spots…

All the best with your investments,

PINNACLEDIGEST.COM

Euro Sun Mining’s Corporate Presentation

Online Resources

Rovina Valley Project Preliminary Economic Assessment, NI 43-101

Disclosure, Compensation, Risks Involved and Forward-Looking Statements:

You must read the following carefully before proceeding.

THIS REPORT IS NOT INVESTMENT ADVICE, NOR A RECOMMENDATION TO PURCHASE ANY SECURITY, NOR IS IT INTENDED TO BE A COMPLETE OVERVIEW OF EURO SUN MINING INC. THE INFORMATION IN THIS REPORT IS NOT A SUBSTITUTE FOR INDEPENDENT PROFESSIONAL ADVICE. SEEK THE ADVICE OF YOUR FINANCIAL ADVISOR AND A REGISTERED BROKER DEALER BEFORE MAKING ANY INVESTMENT DECISIONS.

All statements in this report are to be checked and verified by the reader.

This report may contain technical or other inaccuracies, omissions, or errors, for which Maximus Strategic Consulting Inc., owner of PinnacleDigest.com (“Pinnacle Digest” or “we”), assumes no responsibility. We cannot warrant the information contained in this report to be exhaustive, complete or sufficient. Euro Sun Mining Inc. is a client and sponsor of PinnacleDigest.com. PinnacleDigest.com authored and published this report. Because we are paid by Euro Sun Mining Inc., and therefore we are not independent reporters, our coverage of Euro Sun Mining Inc. features many of its positive aspects, and not the potential risks to its business or to investing in its stock.

Important: Our disclosure for this report on Euro Sun Mining Inc. applies to the date this report was posted on our website (May 7, 2020). This disclaimer will never be updated, even if we buy or sell shares of Euro Sun Mining Inc.

Do Your Own Due Diligence: An investment in securities of Euro Sun Mining Inc. should only be made by persons who can afford a significant or total loss of their investment.

In all cases, interested parties should conduct their own investigation and analysis of Euro Sun Mining Inc. (“Euro Sun” or “the Company”), its assets and the information provided in this report.

The securities of Euro Sun are highly speculative due to the nature of the Company’s plans/objectives and the present stage of Euro Sun’s development, which is in the exploration and development stage. The Company has limited financial resources, no source of operating cash flows and no assurances that sufficient funding, including adequate financing, will be available to conduct further exploration and development of its projects. If the Company’s generative exploration and development programs are successful, additional funds will be required for development of one or more projects. Failure to obtain additional financing could result in the delay or indefinite postponement of further exploration and development or the possible loss of the Company’s properties/projects. A prospective investor should consider carefully the risk factors set out in this disclosure statement and outlined in the Company’s annual and quarterly Management’s Discussion and Analysis, and in other filings made by Euro Sun with Canadian securities regulatory authorities available at www.Sedar.com.

The statements and opinions within this report expressed by Pinnacle Digest are solely those of Pinnacle Digest and not the opinions of Euro Sun. The statements and opinions within this report expressed by representatives of Euro Sun are solely those of the Company and not the opinions of Pinnacle Digest.

Cautionary Note Regarding Forward-Looking Information: This report contains “forward-looking information” within the meaning of Canadian securities legislation (collectively, “forward-looking statements”). All statements, other than statements of historical fact, that address activities, events or developments that Euro Sun or Pinnacle Digest believes, expects or anticipates will or may occur in the future are forward-looking statements. Such forward-looking statements also include, but are not limited to, statements regarding: information with respect to Euro Sun’s expected production from, and further potential of, the Company’s properties; the Company’s ability to raise additional funds; the future price of minerals, particularly gold and copper; Euro Sun having leverage to the price of gold; the estimation of mineral reserves and mineral resources; conclusions of economic evaluation; the realization of mineral reserve estimates; the timing and amount of estimated future production; costs of production; capital expenditures; success of exploration activities; mining or processing issues; currency exchange rates; the ability or likelihood of the Company to get the necessary permits for production; the Company’s development approach to the Rovina Valley Project; permitting advancements; timing of the delivery of the Definitive Feasibility Study; the appointment of engineers; the growth potential of any deposits or trends; any comparisons of Euro Sun’s projects to other mineral projects not owned by the Company; Euro Sun’s future market capitalization; increased investor interest in Euro Sun if the Company can continue to advance the Rovina Valley Project; the gold sector’s potential for entering a period of mergers and acquisitions in the future; the future value given by the market for ‘in-ground’ gold; future valuations for gold projects; government regulation of mining operations; and environmental risks.

Often, but not always, these forward-looking statements can be identified by the use of forward-looking terminology such as “expects”, “expected”, “budgeted”, “targets”, “forecasts”, “intends”, “anticipates”, “scheduled”, “estimates”, “aims”, “will”, “believes”, “projects”, “could”, “would”, and similar expressions (including negative variations) which by their nature refer to future events.

By their very nature, forward-looking statements are subject to numerous risks and uncertainties, some of which are beyond Euro Sun’s control. These statements should not be read as guarantees of future performance or results. Forward-looking statements are based on the opinions and estimates of the Company’s management or Pinnacle Digest at the date the statements are made, as well as a number of assumptions made by, and information currently available to, the Company or Pinnacle Digest concerning, among other things, that the presence of, and continuity of, mineralization at Euro Sun’s projects may not be fully determined; the availability of personnel, machinery and equipment at estimated prices and within estimated delivery times; currency exchange rates; metals sales prices and exchange rates; tax rates and royalty rates applicable to the Company’s project(s); the availability of acceptable financing, and success in realizing proposed operations.

Estimates regarding the anticipated timing, amount and cost of exploration and development activities are based on assumptions underlying mineral reserve and mineral resource estimates and the realization of such estimates may be explained in this report and/or in the Company’s public disclosure documents, including Euro Sun’s Preliminary Economic Assessment prepared by AGP with an effective date of February 20, 2019 (any prospective investor of Euro Sun should read the Rovina Valley Project PEA in its entirety before considering investing in the Company). Capital and operating cost estimates are based on extensive research of the Company, purchase orders placed by the Company to date, recent estimates of construction and mining costs and other factors that are set out in Euro Sun’s filings and disclosure statements found on www.Sedar.com.

Forward-looking statements are subject to a number of risks and uncertainties that may cause the actual results of Euro Sun and/or its subsidiaries to differ materially from those published in the forward-looking statements in this report and, even if such actual results are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, Euro Sun. Factors that could cause actual results to vary materially from results anticipated by such forward-looking statements in this report include, but are not limited to: uncertainties of mineral resource estimates; uncertainties and operational risks pertaining to the Covid-19 pandemic; the nature of mineral exploration and mining; variations in ore grade and recovery rates; cost of operations; fluctuations in the sale prices of products; volatility of gold and copper prices; exploration and development risks; liquidity concerns and future financings; risks associated with operations in foreign jurisdictions; potential revocation or change in permit requirements and project approvals; competition; no guarantee of titles to explore and operate; environmental liabilities and regulatory requirements; changes in project parameters as plans continue to be refined; dependence on key individuals; conflicts of interests; insurance; fluctuation in market value of Euro Sun’s shares; rising production costs; equipment material and skilled technical workers; volatile global financial conditions; conclusions of economic evaluations; legal disputes; currency fluctuations; and other risks pertaining to the mining industry as well as those factors discussed in the section entitled “Risk Factors” in Euro Sun’s Annual and Quarterly Reports and associated financial statements, Management Information Circulars and other disclosure documents filed with Canadian securities regulators. Although we have attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results to differ from those anticipated, estimated or intended.

Forward-looking information contained in this report or incorporated by reference are made as of the date of this report (May 7, 2020) or as of the date of the documents incorporated by reference, as the case may be, and Pinnacle Digest does not undertake to update any such forward-looking information, except in accordance with applicable securities laws. Accordingly, viewers are cautioned not to place undue reliance on forward-looking information due to their inherent uncertainty.

We Are Not Financial Advisors: This report does not constitute an offer to sell or a solicitation of an offer to buy Euro Sun’s securities. Be advised, Maximus Strategic Consulting Inc., PinnacleDigest.com and its employees/consultants are not a registered broker-dealer or financial advisors. Before investing in any securities, you should consult with your financial advisor and a registered broker-dealer.

PinnacleDigest.com is an online financial newsletter owned by Maximus Strategic Consulting Inc. We are focused on researching and marketing for small public companies. This report is intended for informational and entertainment purposes only. The author of this report and its publishers bear no liability for losses and/or damages arising from the use of this report.

Never, ever, make an investment based solely on what you read in an online newsletter, including Pinnacle Digest’s online newsletter, or Internet bulletin board, especially if the investment involves a small, thinly-traded company that isn’t well known.

We Are Biased: Euro Sun is a client of ours (details in this disclaimer on our compensation). We also own warrants of Euro Sun. For those reasons, we want to remind you that we are biased when it comes to the Company.

Because Euro Sun has paid us CAD$200,000 plus GST for our online advertising and marketing services, and we (Maximus Strategic Consulting Inc.) own warrants of the Company, you must recognize the inherent conflict of interest involved that may influence our perspective on Euro Sun; this is one reason why we stress that you conduct extensive due diligence as well as seek the advice of your financial advisor and a registered broker-dealer before considering investing in the Company. Investigate and fully understand all risks before investing.

PinnacleDigest.com is often paid editorial fees for its writing and the dissemination of material. The clients (including Euro Sun) represented by PinnacleDigest.com are typically early or development-stage companies that pose a much higher risk to investors than established companies. When investing in speculative stocks such as Euro Sun it is possible to lose your entire investment over time or even quickly. Euro Sun is not an appropriate investment for most investors.

Set forth below is our disclosure of compensation received from Euro Sun as of May 7, 2020:

Maximus Strategic Consulting Inc., owner of PinnacleDigest.com, has been paid CAD$200,000 plus GST to provide online advertisement coverage for Euro Sun for a ten-month online marketing agreement. Euro Sun paid for this coverage. The coverage includes, but is not limited to, the creation and distribution of reports authored by PinnacleDigest.com about Euro Sun (reports such as this one), as well as display advertisements and news distribution about the Company on our website and in our newsletter. We (Maximus Strategic Consulting Inc.) have bought and sold shares of Euro Sun in the past, and we currently do not own shares of Euro Sun. However, we (Maximus Strategic Consulting Inc.) own warrants of Euro Sun which were acquired by subscribing to Euro Sun’s private placement that closed on March 26, 2019 (click here for private placement details). Any shares we (Maximus Strategic Consulting Inc.) may purchase in the future of Euro Sun will be sold without notice to our subscribers. Maximus Strategic Consulting Inc. may benefit from price and trading volume increases in Euro Sun, and is therefore extremely biased when it comes to the Company.

Junior resource companies such as Euro Sun Mining Inc. are very risky investments: Euro Sun is not an appropriate investment for most investors as it is highly speculative. Risks and uncertainties respecting mineral exploration and development companies are generally disclosed in the annual financial or other filing documents of those and similar companies as filed with the relevant securities commissions, and should be reviewed by any reader of this report. Visit www.Sedar.com to review important disclosure documents for Euro Sun.

It is highly probable that Euro Sun will need to raise additional capital in the future to fund its operations, resulting in significant dilution to its shareholders.

Euro Sun does not have any producing assets, and therefor it has no cash-flow and operates at a loss. Euro Sun may never take any of its projects into production. Even if Euro Sun is able to take any of its projects into production, there is no certainty the Company will generate a profit. Further economic studies, among other types of studies, will be required before Euro Sun is able to make a decision on production. Furthermore, past historical and/or current production in the region of Euro Sun’s projects is not indicative of future production potential for the Company. Any comparisons to other companies or projects may not be valid or come into effect.

Cautionary Note Concerning Estimates of Mineral Resources: This report uses the terms “Measured”, “Indicated” and “Inferred” Resources. United States investors are advised that while such terms are recognized and required by Canadian regulations, the United States Securities and Exchange Commission does not recognize them. “Inferred Mineral Resources” have a great amount of uncertainty as to their existence, and as to their economic and legal feasibility. It cannot be assumed that all or any part of an Inferred Mineral Resource will ever be upgraded to Measured and Indicated categories through further drilling, or into mineral reserves, once economic considerations are applied. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or other economic studies. Viewers are cautioned not to assume that all or any part of Measured or Indicated Mineral Resources will ever be converted into Mineral Reserves. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. Mineral Resource Estimates do not account for mineability, selectivity, mining loss and dilution.

Cautionary Note Regarding United States Securities Law: The securities of Euro Sun Mining Inc. have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”), or any state securities laws and may not be offered or sold within the United States or to, or for the account or benefit of, “U.S. persons,” as such term is defined in Regulation S under the U.S. Securities Act, unless an exemption from such registration is available.

While the information contained in this report has been prepared in good faith, neither Maximus Strategic Consulting Inc. nor Pinnacle Digest, give, have given or have authority to give, any representations or warranties (express or implied) as to, or in relation to, the accuracy, reliability or completeness of the information in this report (all such information being referred to as “Information”) and liability therefore is expressly disclaimed to the fullest extent permitted by law. Accordingly, neither Maximus Strategic Consulting Inc., nor any of its shareholders, directors, officers, agents, employees or advisers take any responsibility for, or will accept any liability whether direct or indirect, express or implied, contractual, tortious, statutory or otherwise, in respect of, the accuracy or completeness of the Information or for any of the opinions contained in this report or for any errors, omissions or misstatements or for any loss, howsoever arising, from the use of this report.

PinnacleDigest.com’s past performance is not indicative of future results and should not be used as a reason to purchase any security mentioned in this report or on our website.

The past performance of Euro Sun’s management, directors, advisors and leadership personnel is not indicative of future results for the Company and should not be used as a reason to purchase any security mentioned in this report.

Maximus Strategic Consulting Inc. and PinnacleDigest.com (including its employees and consultants) are not chartered business valuators; the methods used by business valuators often cannot justify the trading price for most junior stock exchange listed companies, including Euro Sun.

Any decision to purchase or sell as a result of the opinions expressed in this report OR ON PinnacleDigest.com will be the full responsibility of the person authorizing such transaction, and should only be made after such person has consulted a registered financial advisor and conducted thorough due diligence. Information in this report has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete. Our views and opinions regarding the companies we feature on PinnacleDigest.com and in this report are our own views and are based on information that we have received, which we assumed to be reliable. We do not guarantee that any of the companies mentioned in this report (specifically Euro Sun) or on PinnacleDigest.com will perform as we expect, and any comparisons we have made to other companies may not be valid or come into effect.

To get an up to date account on any changes to our disclosure for Euro Sun Mining Inc. (which will change over time) view our full disclosure at the url listed here: https://www.pinnacledigest.com/disclosure-compensation/

Maximus Strategic Consulting Inc., owner of PinnacleDigest.com, does not undertake any obligation to publicly update or revise any statements made in this report.

Learn how to protect yourself and become a more informed investor at www.investright.org

You should refer to Euro Sun’s public disclosure documents found on the SEDAR website (www.Sedar.com) before considering investing in the Company. The public disclosure documents will help investors better understand Euro Sun’s objectives and the risks associated with the Company.

Please be aware and note the date this report was published (May 7, 2020). As a result of the passing of time, the relevancy of the opinions and facts in this report are likely to diminish and may change. As such, you cannot rely on the accuracy and timeliness of the information provided in this report. Since there is no specific guideline as to how long this report may remain relevant, you should consider that it may be irrelevant shortly after its publication date.

Trading in the securities of Euro Sun is highly speculative.