The Greatest Illusion in Finance: How Banks Create Money from Nothing

This article unpacks the hidden mechanics of modern banking, revealing how commercial banks create money out of nothing through credit issuance. It traces the evolution from fractional reserve theory to the revolutionary credit creation theory, exposing how credit expansion—not savings—drives asset booms, inflation, and systemic risk.

Most people believe banks are mere intermediaries - taking deposits from savers and lending them out to borrowers. But what if this widely accepted belief is wrong? What if banks have the power to create money out of nothing? In this article, I trace the evolution of banking theory, uncover a revelation hidden in plain sight, and examine the consequences of a world addicted to credit expansion.

The Lie We’ve All Been Told

For decades, we’ve accepted a simple story: banks take money from depositors and lend it to borrowers. They're the middlemen, financial plumbers ensuring the flow of capital from surplus to scarcity. It's tidy. Intuitive. And wrong.

At least, according to the Bank of England and researchers at the International Monetary Fund.

In the wake of the 2008 financial crisis, the world began to question everything. The housing bubble, the stock market euphoria, the near-collapse of the global financial system - it all pointed to something deeper. Something systemic.

That’s when a 2014 paper dropped a bombshell:

“Banks do not act simply as intermediaries, lending out deposits that savers place with them... but are instead money creators.”

—Richard Werner, "Can banks individually create money out of nothing?"

source: https://www.sciencedirect.com/science/article/pii/S1057521914001070

The truth? Banks create money when they issue loans. And the entire financial system is built on the fragile expansion of credit.

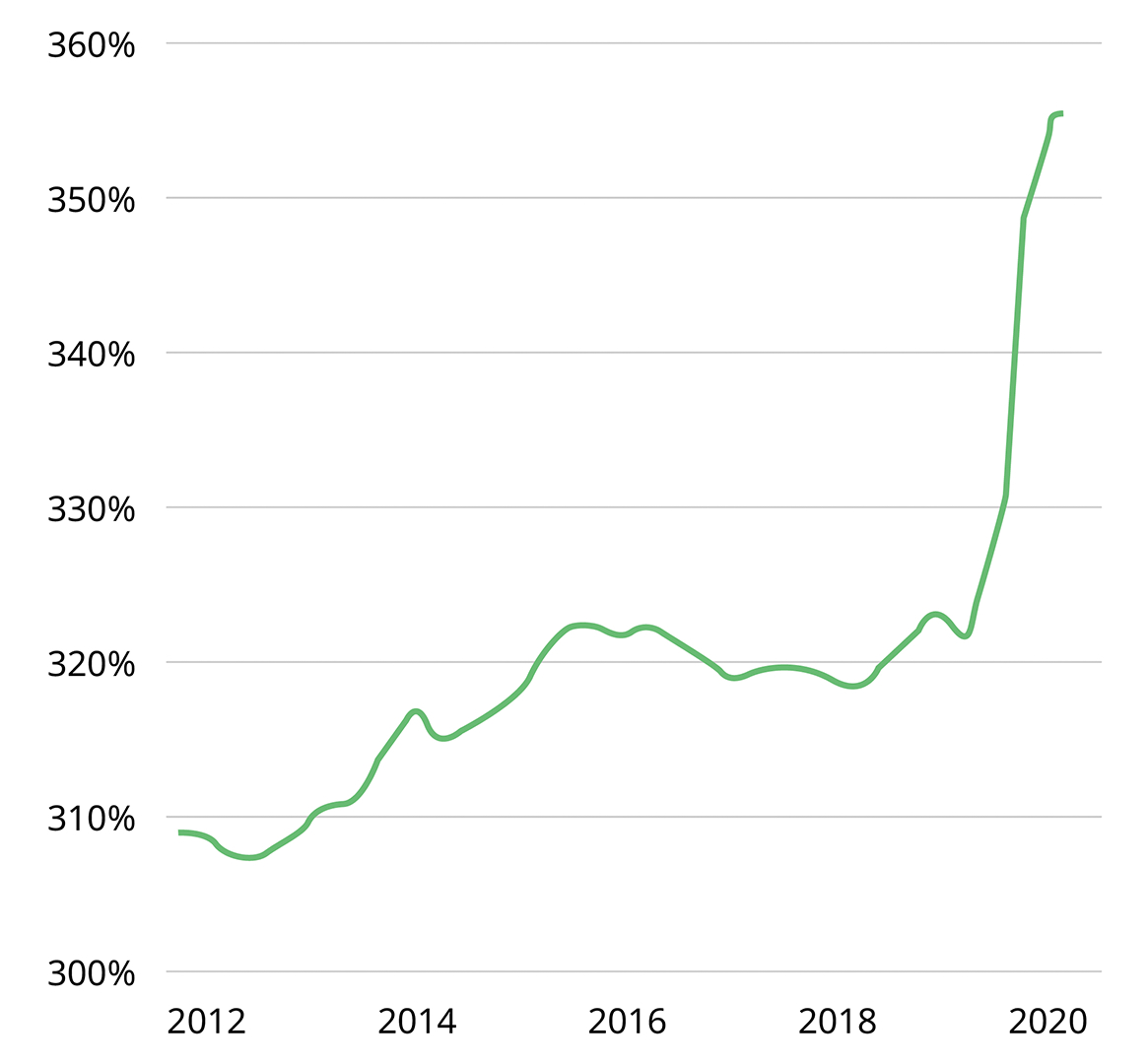

Global Debt As Share Of GDP

The Origins: Fractional Reserve Banking

Let’s go back. Way back.

In medieval Europe, goldsmiths stored gold for merchants and issued paper receipts. Eventually, they noticed that only a fraction of depositors came to claim their gold at any one time. So, they began issuing more receipts - effectively more claims to gold - than the actual gold in their vaults.

Thus was born fractional reserve banking - the foundation of modern finance.

In this system, banks are required to keep only a fraction (say, 10%) of deposits as reserves. The rest can be lent out. And those loans, when deposited elsewhere, become the basis for more loans. This led to the elegant concept of the money multiplier.

The Money Multiplier Myth

Economics 101 textbooks still teach it:

- You deposit $1,000.

- The bank keeps $100 and lends out $900.

- That $900 is deposited elsewhere.

- The process repeats, “multiplying” money.

In theory, a $1,000 deposit can create up to $10,000 in money.

But in practice? That’s not how it works.

The money multiplier assumes banks wait for deposits before lending. But modern banks do the reverse, they lend first and look for reserves later. As the Bank of

England bluntly stated in 2014:

“In reality, in the modern economy, commercial banks create money, in the form of bank deposits, by making new loans.”

—Bank of England, “Money Creation in the Modern Economy”

source: https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creation-in-the-modern-economy

And there it is. It is by making new loans that new money comes into existence.

The Revelation: Credit Creation Theory

Enter Richard Werner, the economist who coined the term Quantitative Easing and author of the pivotal 2014 study, "Can banks individually create money out of nothing?"

He conducted a simple experiment: he borrowed €200,000 from a bank and observed how it was processed on the balance sheet. There was no transfer from other accounts. No reduction in anyone else’s deposits.

Instead, the bank simply created a new deposit in his name - money out of nothing.

“This refutes the model of banking as financial intermediation... instead, each bank is found to create money by crediting the borrower’s account with a deposit, without any prior transfer of funds.”

—Werner, Can Banks Individually Create Money Out of Nothing?

source: https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creation-in-the-modern-economy

In Werner’s Credit Creation Theory, banks are not mere intermediaries. They are money creators, with the unique power to expand the money supply at will, so long as there is demand for credit and the ability to repay. Note the key words 'demand for credit'. This is where central banks come in. We are late in the game now and even a momentary drop in credit expansion, say a short recession could trigger unthinkable consequences to a hyper-leveraged and fragile financial system. The Fed and other central banks must keep the economy humming and credit expanding.

Why It Matters: The Illusion of Wealth

This isn’t just a theoretical shift - it explains the booms and busts of modern capitalism.

- The dot-com bubble of the late 1990s.

- The housing market mania of the early 2000s.

- The everything bubble of the 2020s.

What fueled them? A tidal wave of credit creation.

As banks issued more loans, they injected new money into the economy. That money chased assets from stocks, bonds to real estate, pushing prices higher and higher.

But these weren’t organic increases in value. They were the illusion of wealth, inflated by expanding credit.

“The quantity of money created by banks is the elephant in the room of macroeconomics.”

—Richard Werner

Most people obsess over prices, CPI, interest rates, the price of eggs. But prices are just a symptom. The real driver is the quantity of money. And in our world, that quantity is determined not by savers or even central banks, but by commercial banks issuing loans.

Central Banks: Firefighters or Arsonists?

When crises hit, central banks step in. They cut rates. Inject liquidity. Bail out banks.

But in doing so, they often fuel the next crisis.

After 2008, central banks slashed rates and flooded the system with reserves. But reserves don’t create money. Only bank lending does. So, to stimulate lending, central banks signaled to the world: We’ve got your back.

The result? A decade-long boom in asset prices, record corporate debt, and the illusion of unstoppable growth. Just look at the expansion in debt and deficit spending following 2020.

The truth is: this system works as long as credit expands and that happens to be what central banks know how to do best. The moment it doesn’t, everything begins to unravel.

That’s why central banks fear deflation. It’s not just falling prices - it’s risk of a collapse in the debt-fueled engine of growth.

The Ticking Clock: Can Credit Expand Forever?

Here’s the dilemma.

Our financial system requires constant credit expansion to maintain GDP growth, asset prices, and employment.

But credit has limits.

- Households eventually reach peak debt.

- Corporations borrow to buy back stock, not invest.

- Governments run persistent deficits, monetized by central banks.

What happens when borrowers can no longer borrow, and lenders no longer want to lend?

That’s when the system breaks. Or reinvents itself.

The key question is not whether the system is fragile - it is. The question is: how will they keep it going?

The Future: Engineering More Credit

To sustain the illusion, policymakers have several tools:

- Negative interest rates – Make borrowing cheaper than free.

- Central bank digital currencies (CBDCs) – A way to directly inject credit into the public.

- Yield curve control – Keep long-term rates artificially low to support debt rollover.

- Green energy & infrastructure initiatives – Politically palatable excuses for massive new lending.

- Universal Basic Income (UBI) – Potentially funded via monetary financing, not taxes.

The goal? Keep the credit engine running. Because the alternative, a deflationary collapse of the money supply, is politically and economically unthinkable.

Conclusion: The System We Live In

You don’t need a conspiracy theory to understand modern finance. Just a willingness to see past the smoke screens and what we've always been told.

Banks are not neutral intermediaries. They are the source of new money in our system.

And every time a loan is issued, be it a mortgage, a student loan, a margin account and a new digital dollar is born.

The wealth we see in markets is not always real. It’s often a mirage, backed not by savings or productivity, but by ever-expanding credit. As the real purchasing power of dollars fade and decline, asset valuations soar... but, are we really any richer?

The system functions… until it can’t.

So the question every investor, policymaker, and citizen must ask is simple: How much longer can we grow the illusion? And what happens when it ends? For myself, it means not being beholden to any single fiat currency or banking system. Diversify geographically and understand the assets you hold.

Sources:

Richard Werner, Can Banks Individually Create Money Out of Nothing? – The Theories and the Empirical Evidence, International Review of Financial Analysis (2014)

https://www.sciencedirect.com/science/article/pii/S1057521914001070

Bank of England, Money Creation in the Modern Economy, 2014

https://www.bankofengland.co.uk/quarterly-bulletin/2014/q1/money-creation-in-the-modern-economy

Latest Insights

Recent Highlights from Our YouTube Channel

Comprehensive reviews of current market dynamics and the latest trends influencing the future of investments.