The Strong Dollar, Strong Gold Paradox: When Momentum Breaks the Rules

This article breaks down the unprecedented divergence between gold’s record momentum and a strong U.S. dollar, revealing how market psychology, debt, and central-bank behavior are rewriting the rules of global finance.

In financial markets, some relationships seem almost sacred.

A strong dollar keeps gold in check; a weak dollar lets it run. For decades, this inverse correlation guided investors through cycles of boom and bust — an unspoken law of global capital.

But in 2025, that law has been shattered.

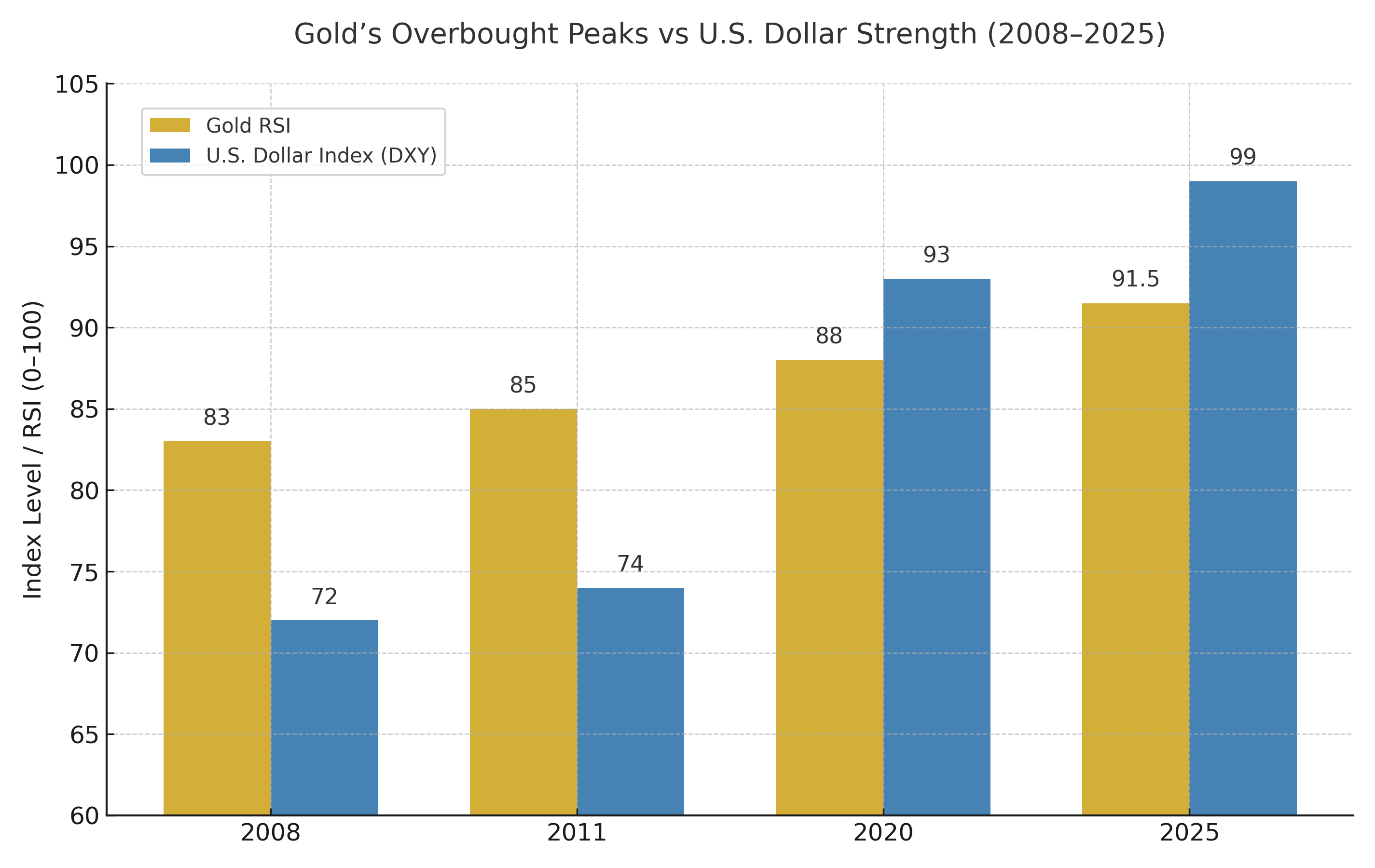

Gold’s monthly Relative Strength Index (RSI) has reached 91.5, the highest reading in 45 years of data. Reaching nearly the same levels as the 1980 mania, but neither the 2011 gold rush, or the 2020 pandemic surge broke 90. Meanwhile, the U.S. Dollar Index (DXY) sits near 99 — its strongest level since 2022.

The message: something deeper than currency weakness is driving gold’s momentum. The metal isn’t rallying because the dollar is falling. It’s rallying despite the dollar’s strength — a sign that investors are no longer measuring gold merely in dollars, but in trust.

RSI: A Barometer of Market Emotion

The Relative Strength Index — RSI — is one of those deceptively simple tools that reveals how human markets truly are.

It measures the speed and magnitude of recent price movements on a 0–100 scale. Readings above 70 suggest “overbought,” below 30 “oversold.”

Gold hitting 91.5 on a monthly RSI means its momentum is nearly off the charts. By comparison:

2008: RSI ~83 — the pre-crisis commodity boom.

2011: RSI ~85 — gold hit $1,920/oz amid QE and debt-ceiling drama.

2020: RSI ~88 — pandemic stimulus flooded global liquidity.

2025: RSI ~91.5 — and the dollar remains strong.

Normally, such readings would signal exhaustion. Yet, in macro terms, the pattern is far more profound: the gold market is expressing the same emotion that equity traders, bond buyers, and even central banks feel — a mix of anxiety and resignation that the “safe” assets no longer hedge what matters most: currency debasement.

The Dollar Disconnect

The U.S. Dollar Index (DXY) tracks the greenback against a basket of major peers — the euro, yen, pound, Canadian dollar, Swedish krona, and Swiss franc. Historically, a falling DXY has been the oxygen for every major gold rally.

The visual contrast (as shown in the chart above) tells the story: gold’s overbought peaks used to coincide with dollar weakness. Now, that inverse link is gone.

This isn’t a technical anomaly — it’s a macro shift. The same monetary policies that once suppressed inflation now coexist with record-high global debt, fiscal deficits near wartime levels, and persistent geopolitical fragmentation. Investors aren’t waiting for the dollar to weaken to hedge systemic risk — they’re hedging against the system itself.

The Macro Mechanics Behind the Break

How can gold rally when the dollar is strong?

Three intertwined dynamics explain it:

1. Global Capital Is Hedging Policy Failure, Not Currency Moves

In past decades, a strong dollar signaled confidence in U.S. policy.

Today, it reflects something different: global demand for short-term liquidity, not long-term trust. The dollar remains the world’s clearing currency, but the assets backing it — Treasuries — are losing their risk-free mystique.

As fiscal deficits spiral above 6% of GDP, investors are parking in cash or bullion — the only assets not requiring political faith. Gold is rallying because the dollar is strong, not in spite of it. The world is hedging both sides of the same coin: liquidity and solvency.

2. Central Banks Have Become the Bid

Since 2022, central banks — particularly in the BRICS bloc — have been net buyers of over 1,000 tonnes of gold annually, the fastest accumulation pace on record. Their motive isn’t short-term speculation; it’s balance-sheet insurance.

For nations on the periphery of the dollar system, owning gold is no longer about profit — it’s about sovereignty. The dollar may still dominate trade, but in reserves, gold is the only asset immune to sanctions, freezes, or counter-party risk.

3. Financialization Has Supercharged Gold’s Volatility

Gold ETFs, futures, and algorithmic trading have turned what was once a slow-moving store of value into a momentum asset.

With algorithmic strategies making up 70–80% of trading volume, even “safe haven” moves are amplified. When gold breaks out, quant systems pile in — pushing RSI readings to extremes that would have been impossible in the manual-trading era.

A Historical Mirror: The 1970s vs. Today

In 1980, when gold peaked near $850/oz, the U.S. was emerging from a decade of double-digit inflation, Cold War spending, and collapsing trust in monetary policy.

The monthly RSI then reached the high-80s, the previous record.

Fast-forward 45 years, and the conditions rhyme, not repeat.

Inflation is milder, but stickier.

Real yields are higher, but unsustainable.

Fiscal discipline has evaporated.

The crucial difference? In 1980, gold’s strength followed a collapsing dollar (DXY fell below 85).

In 2025, gold’s strength is occurring with the dollar at 100. That’s not just rare — it’s unprecedented.

RSI as a Monetary Sentiment Gauge

RSI isn’t just a technical indicator anymore; it’s a thermometer for global psychology.

When the monthly RSI for gold pushes beyond 90, it doesn’t mean a top is imminent — it means the consensus belief in fiat stability is breaking down.

In past cycles:

2008’s RSI spike came before the Fed’s balance sheet quintupled.

2011’s spike came before a decade of negative real rates.

2020’s spike came before $6 trillion in pandemic stimulus.

2025’s spike… we don’t yet know what comes next — but history implies a policy pivot or currency reset usually follows.

The U.S. Dollar’s Paradoxical Strength

It’s tempting to read the DXY near 100 and assume global faith in the dollar is intact. But the index measures the dollar against other fiat currencies — not against real assets.

In that context, it’s like comparing one leaky boat to another.

In real terms — relative to gold, commodities, and even U.S. equity valuations — the dollar is weakening structurally. Its purchasing power, adjusted for CPI, has fallen by over 85% since 1971, when the U.S. abandoned the gold standard.

So while the DXY looks strong on paper, investors are waking up to the fact that “strong” doesn’t mean “sound.”

What the Chart Really Shows

The chart above comparing gold’s RSI and the DXY captures this perfectly.

In 2008, 2011, and 2020, gold’s peaks were tied to a weakening dollar.

In 2025, gold’s RSI has broken all historical records even as the DXY remains firm — meaning gold’s rally is not dollar-driven, but trust-driven.

In plain terms:

Gold is no longer the anti-dollar — it’s the anti-debt. It's investors and regular people opting out of the central bank, government-controlled fiat system.

That’s the key to understanding today’s macro landscape. Central banks, hedge funds, and even retail investors are all reacting to the same underlying truth:

When money supply expands faster than productive output, the value of cash — no matter how “strong” the index says it is — decays.

Implications for Investors

This isn’t a call to buy or sell gold — it’s a call to re-think what gold represents.

Momentum Can Be Rational: A 91 RSI doesn’t necessarily mean a blow-off top. When structural debt, deficits, and geopolitical risk all converge, even a “technically overbought” asset can remain bid for years.

The Dollar Is a Mirror, Not a Measure: A strong DXY today reflects relative weakness elsewhere — the eurozone’s stagnation, Japan’s yield curve control, and China’s deflationary trap. But it tells us little about the dollar’s intrinsic value.

Scarcity Is the New Benchmark: Whether it’s gold, uranium, or lithium, investors are migrating toward assets that can’t be printed. That’s the unifying thesis of this cycle — and the RSI spike is the market’s emotional signal of that migration.

A Turning Point in Market Psychology

Markets are stories — and for half a century, the dominant story was that the dollar was the ultimate truth. Every price, every trade, every valuation started there.

But that narrative is eroding. The surge in gold’s momentum, the record central-bank buying, the flight into tangible scarcity — these are symptoms of a collective realization: the world no longer trusts promises; it trusts proof.

As one veteran trader put it, “The dollar isn’t collapsing — confidence is.”

Beyond Correlation: The Era of Absolute Value

For 45 years, investors have relied on a simple formula:

Weak dollar → buy gold.

Strong dollar → gold stalls.

That rulebook just burned.

Gold’s RSI at 91.5 and a very strong dollar is something no one has seen before. The message for investors is clear:

In a world of infinite money, even the strongest currency can’t suppress the value of the finite.

Gold’s rally is no longer about the dollar — it’s about belief in something real, something which cannot be multiplied. And once belief shifts, the status quo and historical charts become irrelevant.

Latest Insights

Recent Highlights from Our YouTube Channel

Comprehensive reviews of current market dynamics and the latest trends influencing the future of investments.